Alerts

How Manufacturers Can Take Advantage of the Inflation Reduction Act

May 02 2023

The Inflation Reduction Act (the “IRA”) is a wide-ranging bill that includes, among other things, significant investments and reforms by the federal government in a variety of different sectors, including manufacturing, electric vehicles, tax reform, increased funding to the IRS, prescription drug pricing reform, clean energy credits, and substantial funding for various Department of Energy loan and grant Programs.

In this article, we have summarized the key provisions of the IRA for manufacturers who are looking to take advantage of the IRA’s new and/or enhanced tax credits. While there are other tax credits, loan provisions, and grants available under the IRA, including a significant increase in clean energy tax credits for developers and producers of clean energy, those incentives are beyond the scope of this article, which focuses on the following manufacturer incentives:

The IRA revises Section 48C of the Internal Revenue Code to provide a new allocation of up to $10 billion in tax credits for investments in projects that reequip, expand, or establish certain energy manufacturing facilities for the production or recycling of renewable energy property, energy storage systems and components, or other energy property. In addition to providing the $10 billion allocation, the IRA also significantly expands eligibility for the tax credits provided under Section 48C to cover industrial or manufacturing facilities that produce or recycle various renewable energy components not previously eligible, including:

For electric vehicle manufacturers and their suppliers, these additional categories provide the opportunity to receive a substantial credit on investment in new or existing facilities, provided that the manufacturer satisfies the prevailing wage and apprenticeship requirements detailed below.

Notably, to receive the Advanced Energy Project Credits, manufacturers must apply to the IRS for an allocation of the Section 48C credit. The IRS has 180 days from the enactment of the IRA (by February 12, 2023) to establish a program to consider and award certifications to qualified investments. Successful applicants for certification will have two years from the date the IRS certifies their project to prove that they satisfied the certification requirements and that the project has been placed in service.

$4 billion of the $10 billion in allocated credits is intended to go to manufacturers whose factories are located in a census tract where a coal mine has closed or a coal-fired electric generating unit has been closed since December 31, 1999. Manufacturers who locate their facilities in these census tracts are more likely to successfully obtain an allocation of the tax credits and this provision is intended to assist those communities that have been hit hardest by the shift away from fossil fuels.

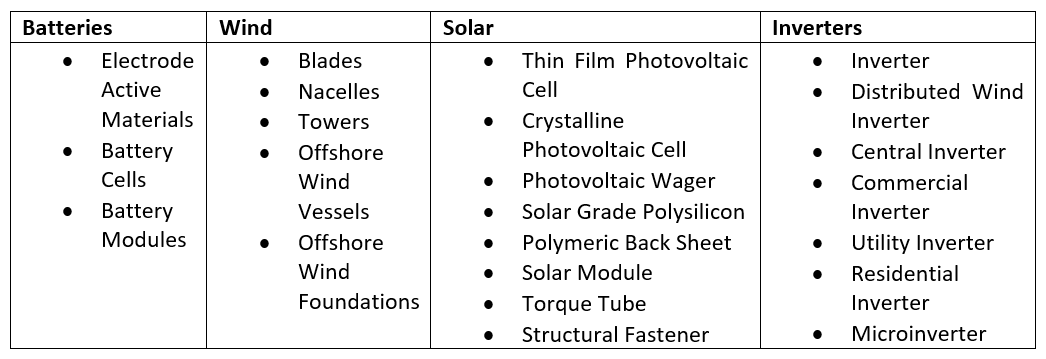

The IRA also creates a new tax credit for eligible components of renewable energy production equipment, including solar, onshore and offshore wind, batteries, and inverters. This credit, available under the newly created Section 45X of the Internal Revenue Code, is limited to production of eligible components in the United States and applies to components sold by a manufacturer to an unrelated person.

The amount of the credit under Section 45X varies by component and the credit is available to qualifying components that are produced and sold after December 31, 2022, with phaseouts of the credits beginning in 2030. Eligible components are included below:

Section 45Q of the Internal Revenue Code is amended by the IRA to increase the incentives available to taxpayers who own carbon capture equipment at their industrial facilities and extend the eligibility for the Section 45Q tax credit to projects that start construction prior to 2033. The value of the credits for captured metric tons of carbon increased as follows:

To take full advantage of the enhanced credits, the taxpayer must satisfy the prevailing wage and apprenticeship requirements (detailed infra) found throughout the IRA. The IRA also significantly reduced the overall amount of metric tons of carbon that industrial facilities must capture in order to qualify for the Section 45Q tax credit down to 12,500 metric tons/year (down from 25,000 metric tons/year for industrial qualified facilities emitting less than 500,000 metric tons/year).

Finally, the IRA revises Section 45Q to allow taxpayers to receive direct cash payments of the Section 45Q credits (instead of receiving a tax credit) and further allows for taxpayers to transfer their Section 45Q tax credits in exchange for cash.

In addition to the various tax credits discussed above, the IRA also substantially increased the amount of funding available to the Department of Energy to loan out pursuant to its Advanced Technology Vehicles Manufacturing (“ATVM”) Direct Loan Program. Specifically, the IRA removed the previous $25 billion cap on the total amount of ATVM loans that the Department of Energy could issue and provided approximately $3 billion in credit subsidy which is estimated to allow the Department of Energy to provide approximately $40 billion in additional loan authority.

Pursuant to the IRA, the Department of Energy can now issue loans for a wide variety of advanced technology vehicles, as well as their component parts. Medium and heavy-duty vehicles, locomotives, maritime vessels, aviation, and hyperloop vehicles are all eligible under the newly-expanded AVTM program.

Typically, manufacturers receiving loan funding pursuant to the ATVM loan program through the Department of Energy will not be precluded from receiving additional state and local discretionary incentives, as the IRA does not preclude such additional funding as a condition of obtaining ATVM loans.

As noted above with respect to the Advanced Energy Project Credits and the Carbon Capture Credits, manufacturers will need to satisfy additional prevailing wage and apprenticeship requirements to take full advantage of the new and enhanced credits provided under the IRA. Specifically, manufacturers will need to:

Pursuant to guidance issued by the IRS on November 30, 2022, the prevailing wage requirements will apply to facilities that begin construction after January 29, 2023, and those requirements are satisfied when:

(1) The taxpayer satisfies the Prevailing Wage Rate Requirements (found at https://sam.gov/content/wage-determinations) with respect to any laborer or mechanic employed in the construction, alteration, or repair of a facility, property, project, or equipment by the taxpayer or any contractor or subcontractor of the taxpayer; and

(2) The taxpayer maintains and preserves sufficient records, including books of account or records for work performed by contractors or subcontractors of the taxpayer, to establish that such laborers and mechanics were paid wages not less than such prevailing rates, in accordance with the general recordkeeping requirements under I.R.C. § 6001 and I.R.C. § 1.6001-1.

If no prevailing wage is available on the website, the taxpayer can email the Department of Labor to request a determination of the applicable prevailing wage. The email address for such requests is [email protected]. The taxpayer should include in the request to the Department of Labor the type of facility, facility location, proposed labor classifications, proposed prevailing wage rates, job descriptions and duties, and any rationale for the proposed classifications.

The IRS’ guidance further specified that the apprenticeship requirements will apply to facilities that begin construction after January 29, 2023, and are satisfied when:

(1) The taxpayer satisfies the Apprenticeship Labor Hour Requirements, subject to any applicable Apprenticeship Ratio Requirements;

a. As set forth above, the taxpayer must hire qualified apprentices for at least 10 percent of the labor hours spent on facility construction, alteration or repair work for 2022, 12.5% of the labor hours spent on facility construction, alteration or repair work for 2023, and 15% of the labor hours spent on facility construction, alteration or repair work for 2024 or thereafter;

b. The taxpayer must also satisfy apprentice/journeymen ratios if the taxpayer or their contractor employs four or more individuals to perform construction work on the project; the taxpayer should meet the ratios applicable with to each entity’s program standards.

(2) The taxpayer satisfies the Apprenticeship Participation Requirements; and

(3) The taxpayer complies with the general recordkeeping requirements under I.R.C. § 6001 and I.R.C. § 1.6001-1, including maintaining books of account or records for contractors or subcontractors of the taxpayer, as applicable, in sufficient form to establish that the Apprenticeship Labor Hour and the Apprenticeship Participation Requirements have been satisfied.

If you have any questions regarding the IRA and whether your company may be able to take advantage of the new and enhanced tax credits it provides, please contact Whit McGreevy.

1 Increased to 12.5% for facilities where construction begins in 2023 and 15% for facilities where construction begins in 2024 or later