Alerts

On Wednesday, the Securities and Exchange Commission (the “SEC”) proposed new rules requiring public companies to disclose the relationship between executive compensation and company financial performance.[1] These rules are long awaited as they were mandated in 2010 under Section 953(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The proposed rules generally would apply to all issuers, including smaller reporting companies, but exclude foreign private issuers and emerging growth companies. The comment period for these proposed rules will expire 60 days after publication in the Federal Register. Although it is not clear when final rules will be adopted, companies should be prepared to implement pay for performance disclosures as soon as next proxy season.

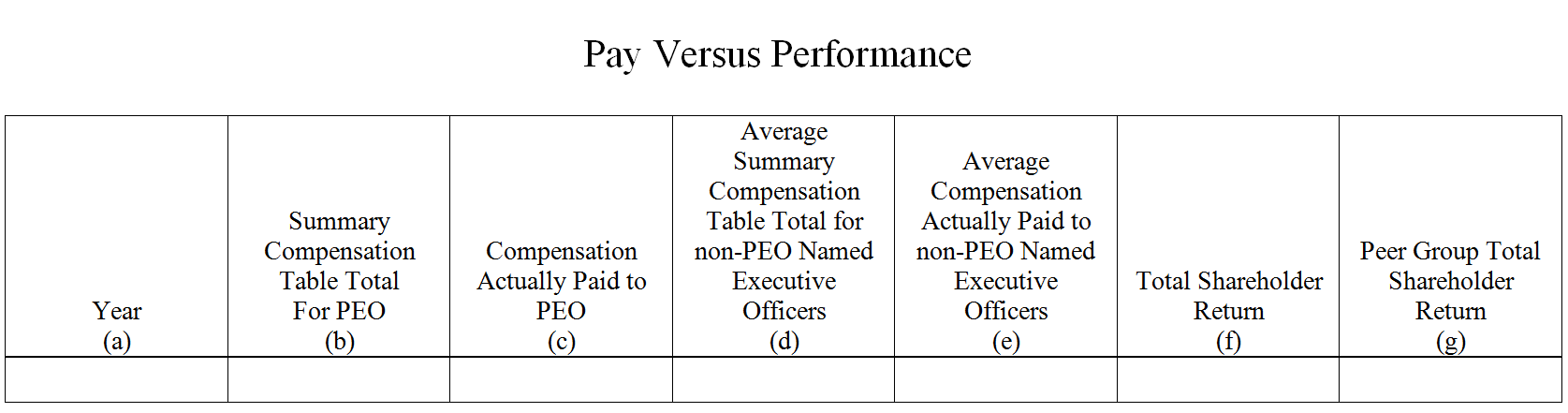

The proposed rules would add a new table (under Item 402(v)) to the executive compensation disclosures required under Regulation S-K in proxy and information statements. This Pay Versus Performance table would require disclosure of (i) CEO total compensation as reported in the Summary Compensation Table (the “SCT”), (ii) CEO actual compensation, (iii) average compensation of all NEOs (excluding the CEO) as reported in the SCT, (iv) average actual compensation paid to all NEOs (excluding the CEO), (v) total shareholder return (“TSR”) and (vi) peer group TSR. The “actual compensation” amounts required to be reported would not include the actuarial value of pension benefits not earned in the applicable fiscal year and would include the fair value of equity awards at vesting (rather than grant). Companies would be required to footnote each amount deducted from and added to the total compensation numbers as reported in the SCT to achieve the “actual compensation” figures reported in this table. The peer group would be required to be either the peer group used in a company’s proxy Compensation Disclosure & Analysis (“CD&A”) or the peer group used in the five-year stock performance graph (under Section 201(e) of Regulation S-K).

A sample Pay Versus Performance table as proposed by the SEC is below:

In addition to tabular disclosures, the proposed rules would also require companies to describe (i) the relationship between executive compensation actually paid and company TSR and (ii) the relationship of the company’s TSR to that of a peer group. These disclosures would follow the Pay Versus Performance table and could be in narrative or graphic form (or a combination thereof).

The SEC has not proposed a specific location for these new disclosures but suggests that the CD&A may be appropriate; however, they note such inclusion may suggest that the company considered the pay-for-performance relationship, which may not be the case, so companies should carefully consider the implications of where the disclosure appears in their proxy statements.

As presently drafted, the Item 402(v) disclosures would be required for the past five fiscal years. However, a transition period would allow companies to only disclose three years’ worth of data in their first year of reporting, and add an additional year of disclosure in each of the next two years, until a total of five year historical data is provided. Smaller reporting companies would only be required to report data for the previous three fiscal years and would be given a one year phase-in period in which they only need to report data for the past two fiscal years. In addition, smaller reporting companies would not be required to disclose peer group TSR or any amounts related to pensions for purposes of disclosed actual compensation amounts. As proposed, Item 402(v) disclosures would be required to be tagged using the eXtensible Business Reporting Language (XBRL) format.

Considerations

Companies should consider their CEO and NEO compensation in light of the upcoming disclosure requirements. In particular, companies should begin to analyze why and how their SCT reported compensation could vary from the actual compensation reported in the Pay Versus Performance table. As the SEC may adopt changes to the proposed rules before declaring them final and it is unknown when these rules will take effect, companies should closely monitor SEC rulemaking for adoption of final rules.

If you have any questions about the proposed pay for performance rules or other securities compliance matters, please contact the principal drafter of this alert, Janet D. Lowder. For further information about Corporate and Securities attorneys, click here.

Womble Carlyle client alerts are intended to provide general information about significant legal developments and should not be construed as legal advice regarding any specific facts and circumstances, nor should they be construed as advertisements for legal services.

IRS CIRCULAR 230 NOTICE: To ensure compliance with requirements imposed by the IRS, we inform you that any US tax advice contained in this communication (or in any attachment) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed in this communication (or in any attachment).

[1] A link to the press release announcing and text of the proposed rules may be found here: http://www.sec.gov/news/pressrelease/2015-78.html (April 29, 2015).